Disability Insurance

Disability Insurance is a program that provides compensation for a person in case of illness or accident. That is why wages are an important condition for this kind of insurance. It does not matter how the person earns his wages, be it from a permanent job position, a contract, commissions or his own business. What is important is to have income. A person cannot receive an insurance amount (benefit) that is more than his income before the illness. Also, consider that monthly payments for this insurance are not deducted from annual income and the benefit received in case of claim is not taxable. That is why the maximum insurance coverage is to provide a certain percent of income, determined at the moment of signing the contract, usually 65-75%. Of course, the client chooses the amount of the coverage according to what he can afford and is able to pay every month. Monthly payments will depend not only on coverage, but also on the other following conditions:

- Profession. It is clear, that it is more expensive to insure a truck driver than an engineer, who spends all of his time in the office.

- Age. The older the person is the more expensive the insurance is.

- Sex. Life insurance is more expensive for men, than for women; disability insurance is more expensive for women.

- Smoking. Non-smokers’ insurance is cheaper.

- Elimination Period – a waiting period – the period of days which must elapse before Disability Benefit payment become payable – usually 30, 60, 90, 120, 180, 360, or 720 days. The longer the Elimination Period is the cheaper the monthly payment is.

- Benefit Period – for how long an insurance company is going to pay you in case of your illness -usually it is suggested to choose 2 years, 5 years, 10 years or until 65 years of age. The longer the benefit period is the higher the monthly payment will be.

Different combinations of elimination period and benefit period will allow you to choose the most appropriate insurance contract with affordable monthly payments.

The most important term in this kind of insurance is the definition of disability.

The wording of the regular definition looks the following way:

– if as the result of an accident or illness a person is:

- unable to perform the important duties of his regular occupation;

- is not engaged in any other gainful occupation;

- is receiving appropriate physician’s care.

For some selected professions (dentist, lawyer, etc.) there is a version of the wording – own occupation. This will allow a person to gain benefits from the company even if he is employed in another occupation. This supplementary term is included in the contract only for the professions, which require long studies and are highly paid.

As the best condition in the contract is considered the fact that in the future the price of the insurance will never change and insurance contract can be extended automatically up to 65 years of age (and it is possible to have it after 65, too – in case the person keeps working). This kind of contract is called renewable and non-cancelable. Also programs with different features exist. For example, some contracts guaranteed automatic extension but price can be changed not only for you but also for all who have the same profession. Monthly payments, of course, will be less and such kind of contract is called renewable and cancelable.

Both plans provide you the payment in case of illness as well as accidents. The benefits are to be paid out starting from the 30-th day – this is the minimum term – and this type of contract is considered traditional. The client must provide a T-4 slip, Income Tax as well as other papers to verify his income. Should an insurance case occur, you do not have to confirm your income again?

There is also a non-regular insurance plan, under the conditions of which you do not have to verify your income prior to signing a contract. However, you will have to do that with all the necessary papers when you become ill or an accident happens. Although this kind of insurance has smaller benefits compared to a regular one, it may satisfy the person who has just started working and doesn’t have a T-4 in this occupation yet. There are no professional divisions and payments are averaged; however, there are insurance categories depending on the types of cases: whether it is illness or a trauma. It is possible to have benefits in both cases – illness and accident or you can choose to have benefits for accidents only and not have benefits in the case of illness. The second variant of insurance is cheaper and in addition it may be negotiated with the condition that in the case of trauma you will have your payment from the first day. (Remember, traditional contract provides a benefit after the 30-th day). To have a benefit paid from the first day of accident might be very crucial in some situations, especially if there are no reserve funds in your family budget.

No matter what type of a contract it is – traditional or non-traditional – the contract is always based on the amount of your income, which you verify by such papers as T-4s, Income Tax Declaration, etc. However, there may be different situations, and if someone’s business brings in $60,000 gross per year, but after deduction all expenses it is reduced to only $10,000 – the insurance company will insure that person for the $10,000 only. To insure all your expenses related to your business you could buy a different program called Business Overhead Expenses.

If you still want to insure your $60,000 but you can’t do it with a regular contract where you are supposed to show the taxable income, we would suggest you deal with AIG and RBC companies. Those companies provide contracts where calculating benefits are based on gross income, which is verified by your paycheques as well as by a letter from your employer. This is a great opportunity for everybody who wants to get disability insurance!!!

Let’s analyze now who may need such insurance.

People who work and have a permanent position are automatically protected by Workers Compensation (WSIB – Work Safety and Insurance Board). This plan covers all employees in case of an injury that takes place at the workplace (not on the way to and from work), fulfilling actions connected with work responsibilities. If a person becomes disabled after an injury at work, the government will compensate his income. A commission of experts decides whether it is going to be a lump sum payment or monthly payments. Only the employer pays the cost for such insurance. In addition, every employee usually has Employment Insurance – which includes a sickness benefit. That means if something happens to a person outside his work -whether it be illness or a trauma – the government compensates 55% of the employee’s salary ($ 413 per week maximum) beginning from the 15-th day and finishing on the 119-th day of the employee’s disability. Therefore two programs protect people who have a permanent position.

As for contract positioned and self-employed people, they don’t have any kind of protection.

Let’s imagine a situation in which you are going to accept a job offer and have two choices:

– you will be paid $50,000 per year, but you won’t get anything in the case of an illness

– you will be paid $49,000 per year. However, should you have a serious injury, an insurance company will compensate you for your lost income based on the tax-free amount of $35,000 per year, which is approximately equal to $50,000 yearly income before tax deductions.

Which choice, do you think, would be yours? The second one?… Unfortunately such an insurance contract doesn’t exist, and if you are a contractor or a self-employed person, you are responsible for finding an insurance plan that would protect you in the best way. That is why people who work on a contract basis are usually offered a bigger salary compared to people who not only have permanent positions but are also covered by WSIB and Employment Insurance, paid by their employers.

Working on a contract basis you have many possibilities to save on the taxes but it is necessary to put aside some of your money for the payment of shielding mechanisms. Ask yourself for how long you may not be working without damaging your family budget. One week? A month? Two months? A half of a year? Most people who have a mortgage usually answer the question this way: “Not even one day. Even long weekends affect my budget.”

Here are a few statistical facts.

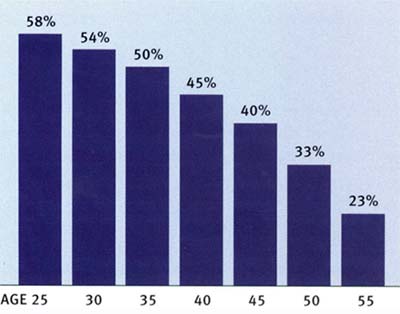

How big is the chance that a person who is before the age of 65 will be disabled for 90 days or longer?

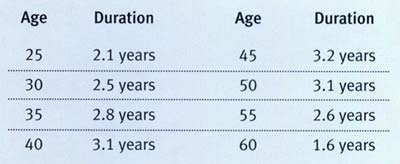

If a person is going to be disabled for 90 days or longer, for how long will it last, on average?

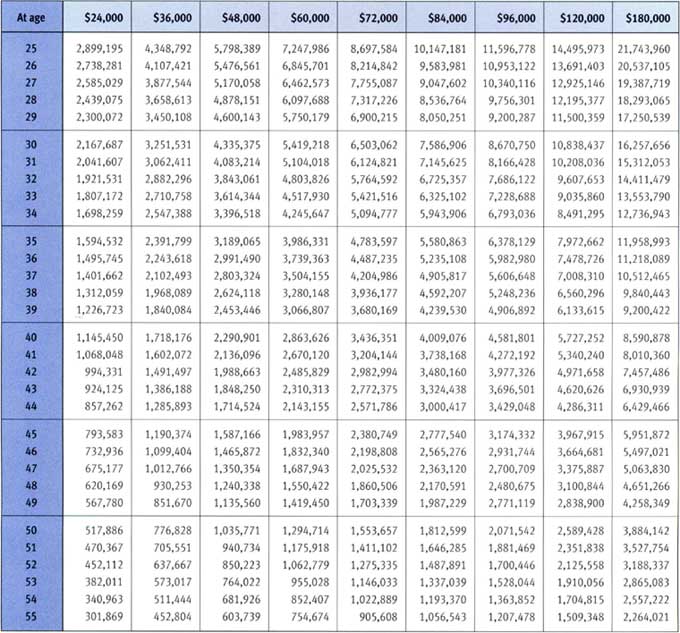

Are you aware of the fact that a big portion of all mortgages is closed for the reason that a family just can’t afford them anymore? According to the statistics, only 4% of mortgages are closed for the reason that the main bread-winner of the family has passed away, but 48% of discontinued mortgages are closed for the reason that the main bread-winner of the family has become disabled. The table below shows how income depends on the age of the income earner. Find your age range and, assuming that the salary of a working person increases 5% annually, determine the percent of family income your family will lose if one member of the family suddenly stops working.

Should you have any questions regarding your particular situation, don’t hesitate to contact me, and I will find an insurance plan that you can afford and that will provide you with adequate protection.